In the previous post we looked at why we need innovation accounting and its definition. This post’s purpose is to understand how innovation accounting is done.

When working on getting an innovation to market, whether while setting up a new company or through an internal project, you first start with an idea. Through a series of experiments you test your idea and refine it until you can reach your goal (usually when starting a new company the goal is to achieve product/market fit).

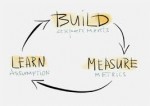

Innovation accounting is the defining, measuring and communicating of this series of experiments. This can be done a number of ways. When using the Lean Startup methodology, it is done through the Build-Measure-Learn process.

Eric Ries’ The Lean Startup book explains in detail the methodology and you can also find over a dozen videos on the web that details how to conduct an experiment. The Javelin experiment board video is a classic. Hence I will only give a brief summary of the methodology here.

Innovation Accounting Step 1: Build

Once you have identified your most critical assumption in your business model (one that must be verified in order for your business to be viable), you design an experiment to test your assumption.

It is important for your assumption to be worded in such a way that it can be validated or invalidated.

The experiment you design must allow you to test your assumption with the least amount of resources possible.

Ideally, your first experiments will be conducted directly with your target market. Either by observing them (ideal), having them act within a specific scenario (also ideal) or by interviewing them (less ideal).

Innovation Accounting Step 2: Measure

When designing your experiment, you will need to determine which metrics will be collected as well as a standard against which you will measure them.

Metrics collected from the web will come from your analytics data. Metrics coming from other sources will most often be collected manually.

Statistically reliable data is not necessary here. You simply need sufficient data to show a direction.

In the context of innovation accounting, your data must be actionable (it must tell you explicitly whether your can pursue your business model in its current form or whether you need to change it) and accountable (you should be able to recreate your experiment at a later date and get similar findings).

Above all, just like it is the case with regular accounting, your experiment must be conducted rigorously, using the highest standards. Otherwise the results of your experiments will be unreliable.

Knowledge in analytics and primary data collection are necessary to conduct valid experiments.

It is important to note here that innovation accounting is a burgeoning discipline. One of the areas that still needs to grow in order to provide better guidelines is how to pick standards for your experiments. At this time, it is left to the market experience of the entrepreneur to determine a standard for an experiment.

Innovation Accounting Step 3: Learn

Learning, while conducting your first experiments, is easy. You have not invested much time or resource in your project yet and backtracking, although not pleasant, can be done easily. As more resources are sunk into the project, pivoting on essential parts of your business model becomes increasingly difficult.

Validating your critical assumptions is the primary goal of your experiments. There is however, a very important secondary goal. That is to keep your eyes and ears open for any other learnings you can pick up along the way. Your early experiments are the ones that will most likely yield the most secondary learnings. Some of these learnings will be so critical that they may impact your business model just as much as not validating your assumption would.

Your innovation accounting log

Drawing a parallel to traditional accounting, you need to keep records of all of your experiments. There are no guidelines established yet showing us how to do this. I will share with you how I keep track of my experiments. Keep in mind that better ways will be developed in the future.

Drawing a parallel to traditional accounting, you need to keep records of all of your experiments. There are no guidelines established yet showing us how to do this. I will share with you how I keep track of my experiments. Keep in mind that better ways will be developed in the future.

Given I am fundamentally lazy and like simplicity above all, I use an Excel spreadsheet to keep a log of my experiments. The variables I keep track of, for each experiment I conduct, are the following:

- Critical assumption

- Market targeted

- Number of participants required

- Summary description of the experiment

- Start date of experiment

- End date of experiment

- Resources required

- What does my minimum viable product consist of

- Metric(s) to be measured

- Standard of the experiment

- Experiment results

- Additional learnings

- Has the critical assumption been validated or not?(color code the cell green or red)

- If not, what is the impact on the business model?

As you fill in your spreadsheet with the results of your numerous experiments, you are tracking innovation. The spreadsheet also serves to show, not only potential investors but collaborators as well, the road you have travelled to get to where you are. Too often it is thought that innovation is born from a single genius idea and a bit of work.

The innovation accounting log shows the size of the effort and the progression of ideas required to bring an innovation to market

Our third and last post of this series will take a look at how innovation options, a disruptive innovation in itself, can determine the maximum market value of an innovation.

You may also like:

The Lean Startup Experiment – Discovery Phase

Lean Startup in the discovery phase – Part 1

The Lean Startup Experiment – Discovery Phase

Lean Startup in the discovery phase – Part 1

Business Experiments: A better way to manage your business?

Business Experiments: A better way to manage your business?

Is Innovation Accounting Going to Change the Way we Do Business?

Is Innovation Accounting Going to Change the Way we Do Business?

Innovation Options: The Game Changer

Innovation Options: The Game Changer

My best business reads for 2015 on marketing, innovation and lean startup

My best business reads for 2015 on marketing, innovation and lean startup